Electric Actuator,Heavy Duty Linear Actuator,Pneumatic Linear Actuator,Micro Linear Actuator Kunshan Zeitech Mechanical & Electrical Technology Co., Ltd , https://www.zeithe.com

Domestic IC self-sufficiency rate increases space, more than 30 production lines stunned the world

The self-sufficiency rate of mainland chips is approximately 25%. With the national policy encouraging the concentration of talent and capital in the semiconductor industry, China's domestic wafer fabrication lines have entered a high-growth phase since 2016. Currently, 17 out of the 22 fabs under construction are expected to begin mass production between the end of 2017 and 2018, with an additional investment exceeding 600 billion yuan.

This article is based on Everbright Securities' report on the mainland foundry industry, analyzing market opportunities and growth paths for local wafer foundries at this key industry transition point. The massive investment of 600 billion yuan presents a significant opportunity for the local semiconductor sector to make a strong comeback.

**Time Node: The Third Transfer of the Semiconductor Industry**

*â–² Semiconductor industry historical migration path*

Semiconductors are often referred to as the "jewel" of the national industry and the "heart" of the information sector. The semiconductor industry originated in the United States, where it still holds a dominant position in design within the IDM model (integrated device manufacturing) and in vertical division of labor. However, memory, wafer foundries, and packaging/testing—areas that require heavy investment and offer lower value—have gradually moved overseas.

Given the high technology and capital intensity of semiconductors, major opportunities typically arise only when there’s a shift in downstream demand. Emerging regions can capitalize on these moments by leveraging technology transfer and lower labor costs to accelerate industrial chain migration.

Historically, two major shifts occurred during the PC and large computer eras. Now, with the rise of IoT (Internet of Things), the mainland semiconductor industry is gaining momentum, creating a critical time window for technological development.

Everbright Securities believes that the next five years will see continued growth driven by increased silicon content in smartphones, while emerging fields like automotive electronics and IoT will be high-growth areas. Supported by national policy funds, the mainland semiconductor industry has become the third wave of global semiconductor industry relocation through accumulated technology and early strategic positioning.

**Local Status: Increasing IC Self-Sufficiency Rate**

*â–² Strong domestic demand and rising IC self-sufficiency rate*

China is the world’s largest semiconductor consumer market, with its share of global semiconductor demand rising from 7% in 2000 to 42% in 2016, acting as the main driver of global market growth. However, the development of the mainland semiconductor industry has not kept pace with its massive market demand, and the country still heavily relies on chip imports.

According to SEMI data, the self-sufficiency rate of local chips was just 25% in 2016, and it is expected to remain below 30% for the next few years. There is still significant room for improvement in the self-sufficiency rate of domestic ICs.

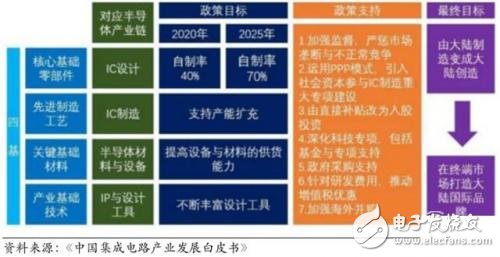

**Trend: Policy Benefits Three Key Segments**

*▲ China’s semiconductor industry policy objectives and support*

To reduce over-reliance on imported chips, the Chinese government has elevated the semiconductor industry to a national strategic level, setting clear goals for design, manufacturing, and testing. The first phase of the National Integrated Circuit Industry Investment Fund (Big Fund) raised 138.72 billion yuan. As of September 2017, over 55 investments had been made, with a total committed amount reaching 100.3 billion yuan. A second phase of fundraising is currently underway.

In addition, local integrated circuit investment funds—inspired by the Big Fund—have reached 514.5 billion yuan, bringing the total fund size to 653.1 billion yuan. These efforts are accelerating capacity building and R&D progress, helping to enhance the competitiveness of the Chinese semiconductor industry.